Intermarket Analysis Throught Macro and Technical Methods

19# Investment Opportunities by Sector Valuations.

Sector Valuations and Opportunities: Trends for the Future.

Here you will find:

- A detailed analysis of all American macroeconomic sectors.

- An analysis of their growth, specifically starting from October 2023.

- The moment when capital rotation between sectors began.

- Relative valuations of all sectors.

- The sensitivity of each sector to macroeconomic factors.

- Where the trading opportunities lie.

Intro

In this article, we’re going to analyze the relative values of sectors within the American economy. We have our own macro view, which we’ve covered here, and we want to identify any valuation that is inconsistent with our hypothesis.

Exploring Investment Opportunities Across Various Sectors

Our macro view is that we are in a macroeconomic slowdown heading towards a recession (here). We know that in each stage of the macroeconomic cycle, sectors perform differently.These particularities are related to the elasticity of the products and services each sector offers.

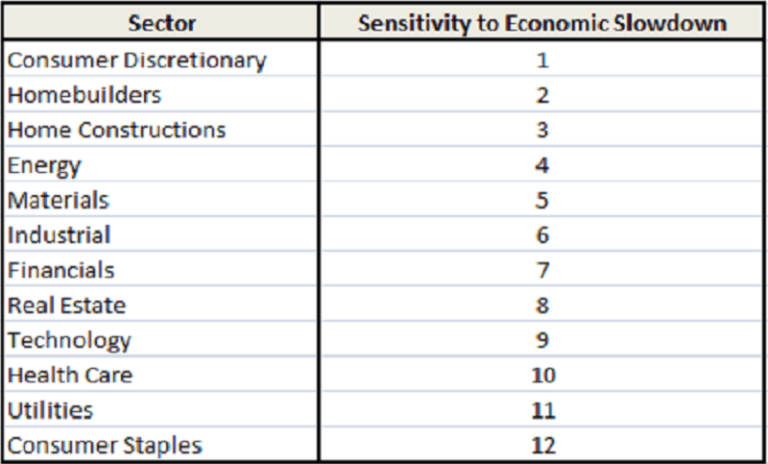

Sectors most exposed to a slowdown/recession are:

*1 = highest sensitivity.

Sector-Specific Investment Opportunities: A Closer Look

A correct diagnosis of the macro view is crucial. It narrows down the range of vehicles, and even if it’s not 100% accurate, it reduces the margin of error. This is because, to a greater or lesser extent, both a slowdown and a recession affect all sectors in the same direction.

Interest Rates

In October 2023, the 10- and 30-year interest rates hit their peak and began to decline. This is a clear market signal (through the yield curve, as we saw here) that future economic expectations are starting to fall. This scenario triggers a rotation of capital into the more inelastic or resilient sectors during a slowdown.

Resilient sectors to the macro cycle:

Utilities, Health Care, Staples.

- Utilities. Their demand varies little because they are essential services like electricity, water, and natural gas.

- Consumer Staples. Food, beverages, cleaning supplies, and household care products.

- Health Care. Health-related products.

Exploring Investment Opportunities Across Various Sectors

In October 2023, all three sectors started a bullish rally. This is no coincidence. As the most sought-after sectors, given their defensive nature during a slowdown, it’s logical that they are in higher demand than usual. The drop in long-term rates is a clear signal of market expectations, as reflected in the yield curve (we covered this here).

Sector by sector.

All sectors are on the same scale. The chart illustrates the growth of each market sector when rates started to fall. The drop in long-term interest rates obviously affects the cash flow of all sectors positively, increasing their valuation. The problem arises when that rate drop reflects a recessionary economy.

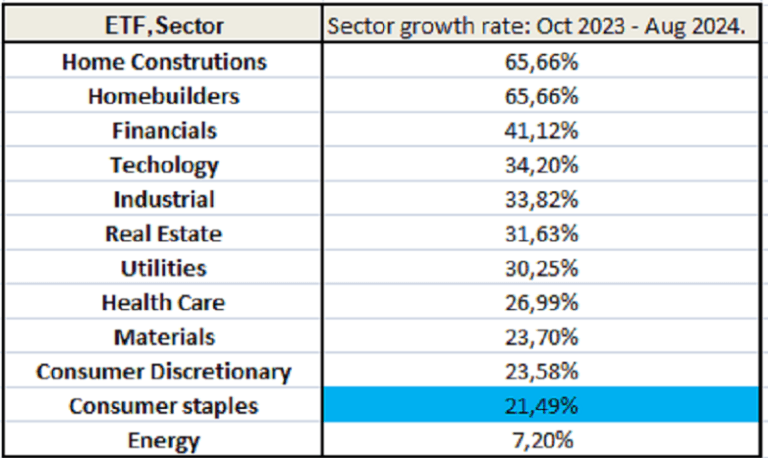

Which Sectors Offer the Best Valuations Today?

The growth of each sector from Oct ’23 to Aug ’24.

*In blue, Consumer Staples.

This growth seems like that of a thriving economy. The sectors that are starting to show signs of slowing down are Consumer Discretionary (as we discussed here, including a technical setup) and the Energy sector (covered here, also with a technical setup).

Macro view

The dilemma arises when those lowered expectations about the future economy become evident in the stock market.

If these expectations were confirmed—and we believe they will—how is it possible that all sectors continue growing?

Sensitivity of each sector to the macroeconomy.

*1 = highest sensitivity.

The only sectors whose growth reflects an economic slowdown are Consumer Discretionary (the most sensitive of all) and Energy (the fourth most sensitive).

Future of Different Sectors: Where to Invest Next?

We’ve been discussing for a while:

- The huge oversupply in the new residential housing market and the inevitable price adjustment coming (covered here).

- Builders with poor inventory management will see their valuations drop, and therefore, the value of the company (covered here).

- The decline in disposable income and its effect on discretionary consumption

- The worst housing affordability conditions in history, exacerbated by rising interest rates

We are facing a market in a state of “irrationality.” We all know that these states can last longer than expected. It’s safer to trade a sector rotation (like trading Health Care and Utilities, as we covered here) than to try to pinpoint a top in an irrational market.

Remember

“The market can stay irrational longer than you can stay solvent.”

Despite this, portfolio management is still possible by readjusting sectors and asset types.

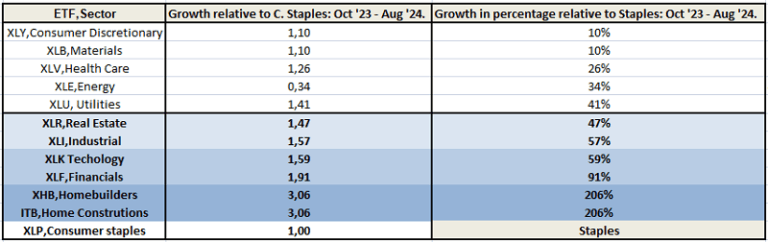

Seeking opportunities: Valuation by comparables.

We compare all sectors in the market with Consumer Staples.

*Growth relative to Staples from lowest to highest between Oct ’23 and Aug ’24. The more shaded, the greater the opportunity.

The context is clear. We have a macro view that is starting to be reflected in discretionary consumption and the energy sector.

However, there are completely overvalued sectors that require portfolio adjustments and, as a result, present opportunities for trading.

If you’ve been following us, you know what we’re trading. We’ve sent setups in Discretionary (here), Health Care (here), Real Estate (here), among others. We believe the rotation is just starting, and we consider it safer to move towards continuity sectors rather than trying to chase irrational tops, which, as we know, can last for a long time.

The setups that emerged from this analysis can be found in the blog, in article #20. If you are already a subscriber, these setups have been sent to you via email.

As always, I hope you enjoyed this as much as I did writing it. I’ve been passionate about my work for nearly 30 years now—a privilege life has granted me.

That’s all for now. Please share this. The subscription won’t cost you anything and it makes our day. You can find us at intermarketflow.com and on X @intermarketflow.

See you soon,

Martin

Intermarketflow.com

- Intermarketflow