Intermarket Analysis Throught Macro and Technical Methods

#23 Commodities Currencies, Evaluating Risks and Rewards

Seeking opportunities in commodity currencies, the dollar, and interest rates.

In this article, we will analyze commodity currencies with different profiles, specifically AUD, CAD, and BRL. We will examine all three under the lens of three distinct macroeconomic contexts determined by the U.S. 2-year interest rate.

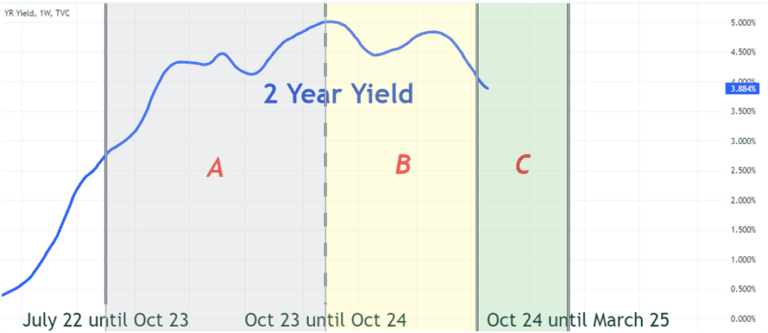

- Context A: Strongly rising rates: +72.28% (July ’22 – October ’23).

- Context B: Falling rates: -28.46% (October ’23 – October ’24).

- Context C: The future until March ’25, where the market currently expects an 8.89% increase in 2 year rates by March ’25.(October ’24 – March ’25)

We aim to investigate the relative strength and sensitivity of these currencies to the Dollar. From there, we’ll examine historical correlations with their respective commodities, looking for anomalies tied to U.S. interest rates, commodity prices, or their correlations. We’re searching for extremes—positive or negative—that are unsustainable over time. This will be contextualized through intermarket analysis (more details here), and as always, we’ll try to identify an opportunity and frame it within technical analysis.

Understanding the Link Between Commodities and Forex

At the center of the diagram, we see interest rates. Implicitly, we’re talking about U.S. interest rates because they have the ability to affect other rates, both sovereign and corporate. In this case, we use the U.S. 2-year rate as a reference.

Commodity Currencies: Different economic contexts using the U.S. 2-year rate.

Commodity Currencies and the U.S. Dollar in Period A.

This period is marked by a significant rise in U.S. interest rates. Between July ’22 and October ’23, the U.S. 2-year rate grew by 72.28%. Using this as a filter, we analyze behaviors and correlations during that period.

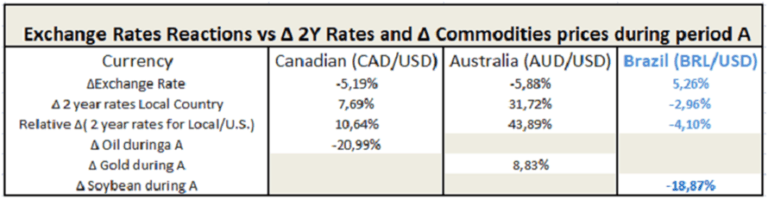

Commodity Currencies in Period A: ∆ U.S. Rate = +72.28%

Of course, U.S. interest rates and commodity prices are not the only determinants of a country’s exchange rate. Macro factors, expectations, and political influences, among

others, also play key roles. However, this is not what we’re focusing on. We may infer these factors but they won’t trigger our trades, simply because the amount of information is endless and overwhelming.

Commodity Currencies During Period A

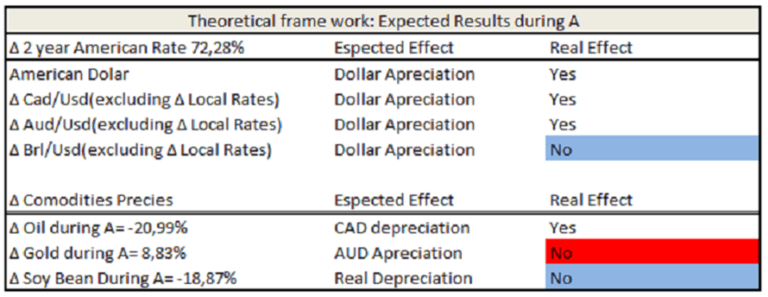

Commodity Currencies: Theoretical framework in A.

· Commodity Currency CAD:

It has a large interest negative rate differential against the U.S. and its main commodity plummeted during the period. The result fits within the theoretical framework, and the impact on the exchange rate could have been greater, considering other variables. This shows some resilience.

· Commodity Currency AUD:

It has a better, still negative, rate differential than CAD, its commodity rose during the period, yet the currency depreciated. It shows greater weakness against the Dollar than CAD. Other factors are affecting and weakening this currency.

· Commodity Currency BRL:

It has the worst rate differential against the U.S., its commodity dropped during the period, yet the currency appreciated against the Dollar. This currency has the highest relative strength and thus the best performance in Period A.

· Reserve Currency: Dollar:

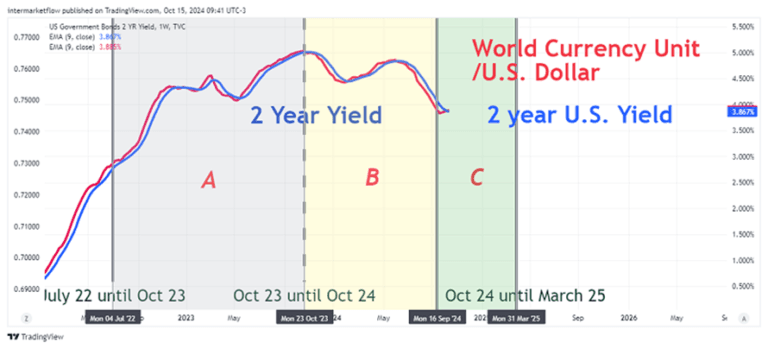

To complete the analysis, look at the correlation between the U.S. 2-year rate and the World Currency Unit measured in dollars. The W.T.O. is an index used by central banks to determine relative valuations between countries. It’s similar to the more popular Dollar Index but includes more currencies, like China.

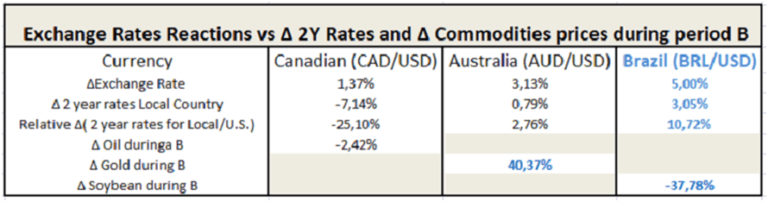

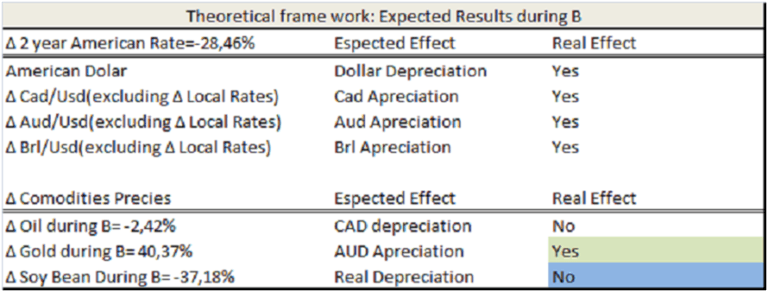

Commodity Currencies and the U.S. Dollar in Period B: ∆ U.S. Rate = -28.46%

Comodities Currencys: Theoretical framework in B.

In this period, marked by a significant drop in U.S. interest rates, we will analyze how commodity currencies behaved and what correlations emerged during the decline. The key focus here is to understand how these currencies reacted to falling U.S. rates,

factoring in the influence of commodity prices and broader macroeconomic trends.

· Commodity Currency CAD:

It has a large interest rate differential in its favor vs. the U.S., with local rates dropping much less. Its main commodity fell by 2.42%. The result doesn’t fit the theoretical framework, but the absolute change is minimal. Despite the favorable rate differential, the CAD barely appreciated, showing weakness in the local

currency.

· Commodity Currency AUD:

It has a massive rate differential in its favor. Australian rates rose nearly 1% while U.S. rates dropped by 28.46%. Additionally, one of its key commodities rose by 40.37%. Despite all these favorable factors, the AUD barely appreciated. Other variables are driving the AUD’s significant weakness, possibly related to trade relations with China or another factor. Regardless, the AUD is by far the weakest of the three currencies under study.

· Commodity Currency BRL:

It has a very strong rate differential in its favor vs. the U.S., with local rates rising by 3% compared to a 28.46% drop in U.S. rates. On the downside, its main commodity dropped by nearly 40%. The net effect, however, was an appreciation of the BRL, once again demonstrating resilience.

Conclusions so far:

- The BRL appears to be the currency most independent from U.S. interest rates and, in these periods, has achieved some independence from its main commodity. We can infer that macro fundamentals, expectations, and macroeconomic policies inspire confidence in the currency.

- This is not the case for either the CAD or the AUD. Particularly the AUD, which failed to appreciate despite a favorable rate differential and a 40.37% rise in one of its main commodities. We can infer that other factors are affecting the currency, potentially related to poor trade expectations with China, among other reasons. However, it’s irrelevant to dive deeper into these factors.

- Setups emerge in situations of extreme strength

and/or extreme vulnerability.

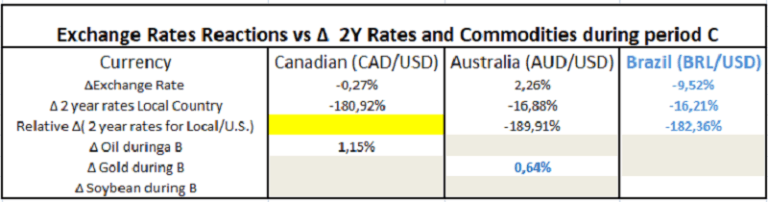

Commodity Currencies and the U.S. Dollar in Period C: ∆ U.S. Rate = +8.89%

The Future.

Period C stands out because it covers October 2024 to March 2025. To continue the analysis, we rely on the futures market for all variables up to March 2025. This gives us the market's current outlook, considering the current terms of trade. While we know this view may be wrong and will likely change, today's prices provide the best available information at this time.

Commodity Currency: AUD.

Still the weakest, this currency is expected to show more rate weakness compared to the U.S., with a stable gold price. Contradictorily, the exchange rate is projected to appreciate, suggesting other factors are driving the currency. However, the negative rate differential is too large to align with the current or expected value by March 2025. The same questions posed for the CAD apply here, but with greater risk. The currency seems influenced by factors unrelated to the rate differential and commodity price, increasing the risk. The analysis will proceed with this in mind.

Commodity Currency: BRL.

It has a strong negative rate differential expected for 2025 and soybean prices at current levels. A 9.52% devaluation is expected based on this rate differential. Another possible setup arises by investigating the questions mentioned above.

Commodity Currencies: Theoretical Framework in C.

To summarize as of today:

- CAD has shown significant weakness and it continues showing it in March 2025.

- AUD has experienced extreme weakness, and this is expected to continue.

- BRL has demonstrated extreme strength, but the interest rate differential for March 2025 does not favor it. The market expects a reversal of this current strength.

Of course, all this information is meaningless without a macro view. We have ours. We’ve discussed it here, and it’s very clear and concrete.

It provides the foundation from which we frame our setups.

We are working on the analysis of potential setups in these three currencies and across different asset classes. Unfortunately, the research is not yet complete, and it will be sent to you next week through this channel. It will also be published on our blog.

Please share this. By the way, the subscription won’t cost you anything and it makes our day!

As always, I hope you enjoyed this. It’s a topic that could be explored much more deeply, especially on a mathematical level with variances, covariances, regressions, etc. But time is of the essence!

Stay in touch. You know where to find us: @intermarketflow or at

intermarketflow.com.

Martin

Intermarketflow.com

- Intermarketflow

Intermarket Analysis LLC

703 Waterford Way - Suite 805 - Miami, Fl 33126

Unlock Full Access

We create professional content for traders, based on intermarket, macro, technical, quant, and flow analysis.

Welcome aboard — enjoy the ride.

If you have already registered before, please enter your email again to recover your session.