Intermarket Analysis Throught Macro and Technical Methods

#38 The small banks: risks and threats they are facing.

Threats and weaknesses of small banks

Here you will find:

1.a Description of the U.S. banking industry, especially the small bank segments.

2. The market share that each type of market has over the different types of loans.

3. Operational processes of small banks and why they expose them.

4. Incentives that small banks have today.

5. The numbers of the credit market in different types of credit. The risk of each type of credit.

6. Where the sources of risk arise.

7. A technical setup, based on stage 3 of the macro narrative, the arguments and prevailing variables for operating in a highly volatile market.

In one of my old jobs, not so long ago, we did balance sheet analysis for a bank. My former boss and now a friend, M.G., taught me that it is not possible to value a company on the basis of its last balance sheet. Not even its last 5 balance sheets.

A company is worth what it’s expected to earn within the ecosystem in which it produces.

Future Trends in Independent Banking

This includes the country in which it operates, the composition of the market and its competitors, its position within that market and future expectations in terms of cash flows.

An E.B.I.T.valuation of x5, x10 or x15, depending on the country in which it operates, can increase or dramatically decrease its value depending on expectations, market trends and, in some cases, its position and pricing power within that market.

The whole ecosystem in which it operates must be understood in order to understand micro behaviour.

So to analyse the current state and value of US retail banks, we first need to understand:

- How the market is structured: how many players there are.

- The competitiveness of their segments, which is defined by the type of product or service they provide (this is defined by the degree of standardisation of their products).

- What products or services they sell in relation to technological advances.

- Are they cutting-edge, do they have the whole market as potential customers, or are they stable products where the market is a repeat, replacement or maintenance market?

- Interaction zones of competition, based on each of their products or services.

All of this defines the floor and ceiling of value.

Understanding Financial Stability in Local Institutions.

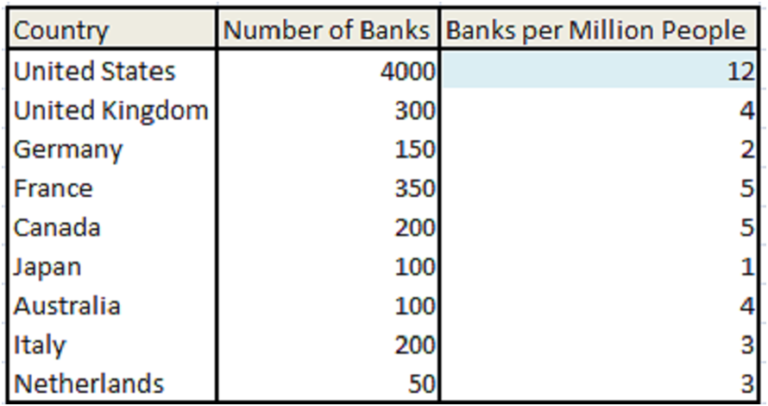

The USsmall bank market: Level of competition, Comparison with developed countries.

In the case of the United States, the 4,000 banks are the institutions insured by the FDI.

None of the countries mentioned above include credit unions, although they are importantplayers in some market segments. For the simple fact that they are not for profit.

- TheUnited States has the most competitive small bank market in the world on a per capita basis. Academics would describe this market as one of perfect competition. That is, the price is given and profitability is defined by the volume they handle. The price is the market price. If you improve it, in theory, you would get the whole market. The opposite is true for monopolies.They adjust quantities that set the price that maximises the monopolist’s profitability. This of course is micro economics 1.

Market participants.

- Large banks.

- Regional banks.

- Local banks.

- Credit Unions

All have different business models with similar products but with totally different structures, commercial networks and technologies.

Future Trends in Independent Banking.

Local and Regional Banks

They have a number of differences of all kinds, in terms of regulations and capital requirements. We could go into each, but I think it is clearer and more understandable to say that small banks generally have only one local branch.They are in their local, small, agricultural towns, far from large urban centers.

Strongly committed to the society they are part of and in fact, this local knowledge is a fundamental asset within their business model.

The difference with a regional bank is that they have branches in several locations, are geographically closer, are larger and aim to finance larger projects. Large banks are the last link, they are in the big cities and finance larger loans.

The credit portfolio they manage has a different profile, type and size of credit, but mainly, they have different back offices, technologies and legal support to manage them.

The entire ecosystem competes today with the emergence of Fintechs in various market segments. Of course, each type of bank has different tools to compete against this new emergence of faster, more efficient and generally cheaper lenders.

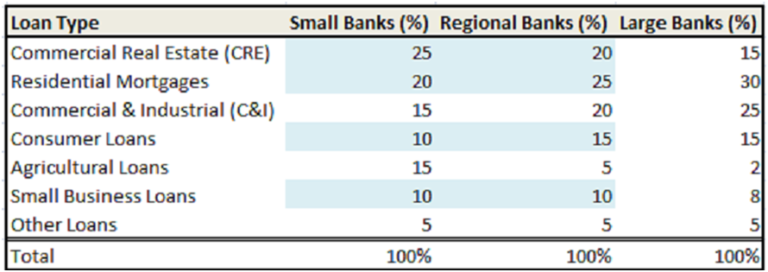

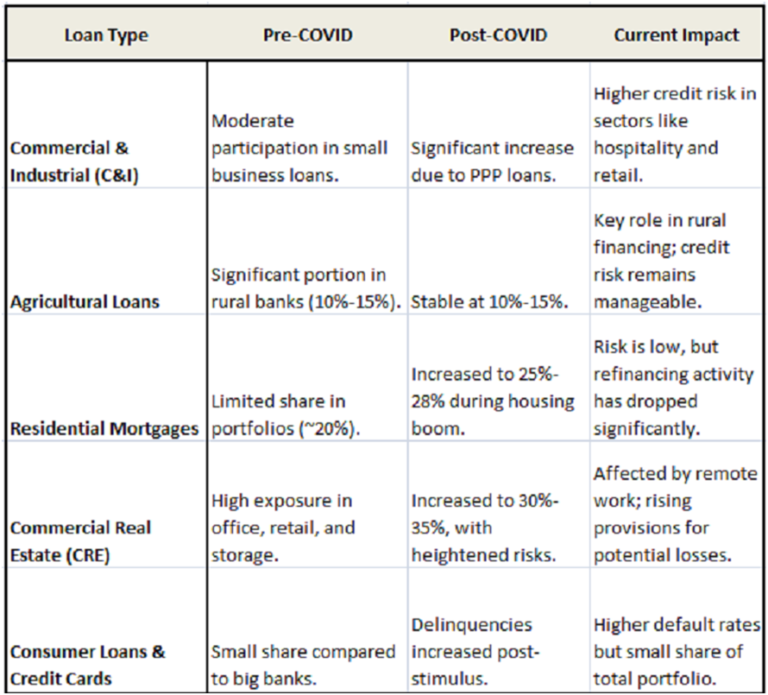

Market share by bank category in the different types of credit.

The business model of each type of bank is illustrated by its share of different types of loans.

Evaluating Stability in Local Lenders: Special Featuresof Local Banks.

A small, local bank has an owner who is in direct contact with the community. He knows their needs and lives in the area. Is the kind of person who walks around his locality and says hello to everyone, and everyone says hello to him. That’s their main asset. They don’t ride in limousines, their children go to the local school and they have a beer in the community bar.

They are in touch with the local municipalities because they are a fundamental part of their development. This is the area where they have the most access and can be anything from a restaurant, workshop, amusement park and commercial premises to multi-family dwellings and offices.

A big bank has too big a hand to get in there, and the regional bank competes, but they don’t have the deep knowledge of that locality or the commercial network to get in there.

Another player would be credit unions, but in general they have different functions.They bring together producers and current businesses with the aim of achieving improvements through joint action.

In addition, when a new business, a local restaurant, a local pub, a local workshop starts up, which bank do you think will knock on the door first?

This is another of the strengths of small banks, the flexibility to adapt.

In several segments of the credit market, regional and local banks have more than 50% of the total national market.

They have a 70% share of real commercial loans and small business loans. Their business model is geared in this direction.

There is a big difference in the way these loans are handled. Because of their size, backoffice, commercial contacts and technology, local banks do not securitise their loans. They have neither the commercial network nor the technology to do so.These assets simply end up on their balance sheet at loan value. This exposes them.

Several conclusions can be drawn from the small bank market.

- They compete on volume because price is determined by perfect competition.

- This creates incentives to increase volume, in order to increase profitability, which is very, very tight. In addition, they have a $200,000 state insurance on their deposits.

- Because of their back office characteristics, technology and commercial networks, their loan portfolio remains in the commercial real estate, commercial, industrial and small business lending segment.

- They do not securitise their loans because they do not have the back office, commercial network or technology to do so, and these loans enter their balance sheets as collateral for the loan.

- The whole industry is in competition with fintech technology which creates economies of scale and can therefore improve prices.

- The reaction function of the central bank is well known. One central bank to save them all!

My boss used to describe this situation “as ‘a shit-smelling swamp”.

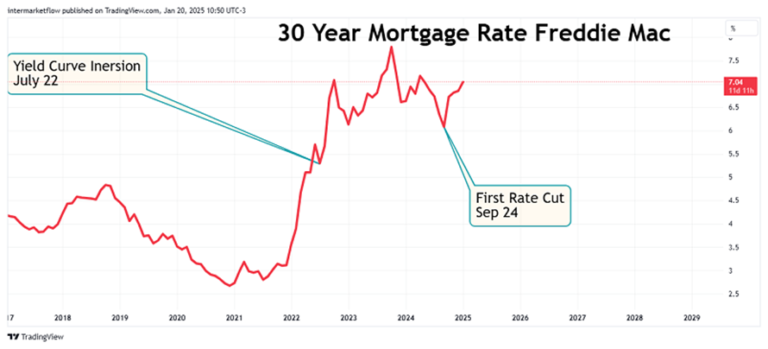

Add to this ecosystem an inversion of the curve on 22 July, a rise in short-term rates and now a rise in long-term rates, and you get these mortgage rates.

By historical standards, it is comparatively expensive to take out a mortgage loan.

Of course, as prices rise, demand for this type of credit falls. This implies that approximately 60% of the small bank’s portfolio sees demand fall. Its flagship products are in decline. This latter graph is at the national level.

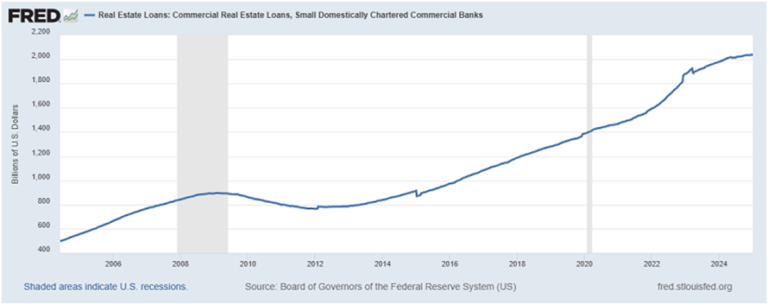

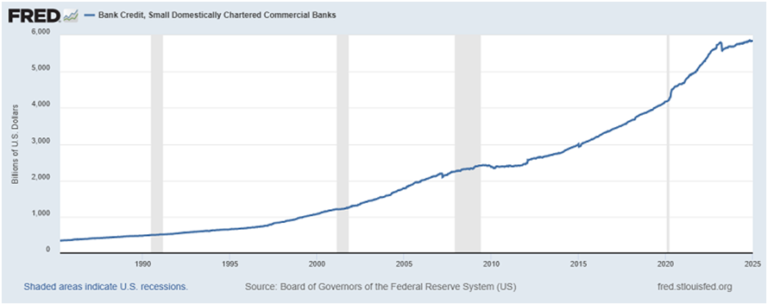

Despite the fact that loans are expensive, lending by small banks continues to rise.Remember that small banks do not securitise their mortgage loans.

Lending by small banks continues to rise. The only difference is that these loans are more expensive and therefore riskier.

Small Bank Deposits.

Deposits in small banks continue to rise at or around the same rate as loans granted, only that these loans are riskier.

Assets in Cash Small Banks.

The sub-regional crisis affected the cash in these banks. Although it recovered somewhat, it never returned to previous levels and would be non-existent if it were not for the existing insurance.

Evolution of small banks’ credit portfolios.

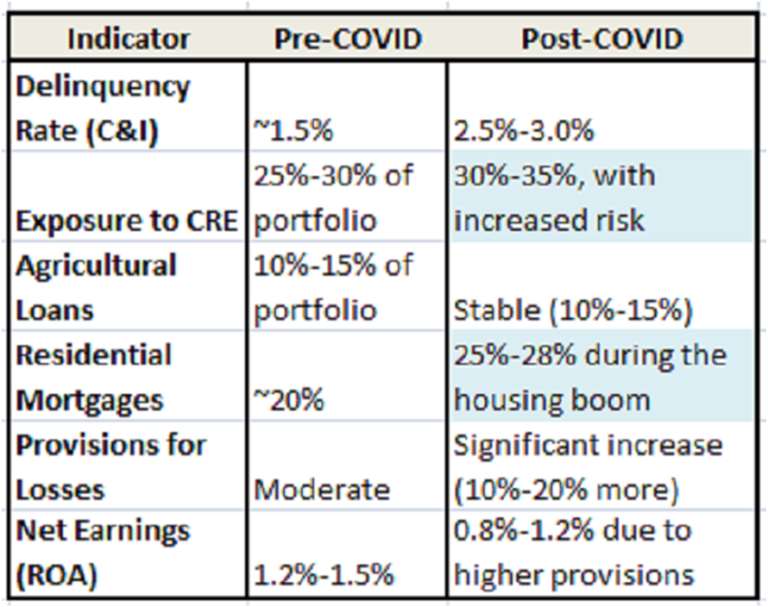

Key Indicators.

Delinquency Rates U.S.

The rise in delinquency rates goes hand in hand with the increased riskiness of new loans.

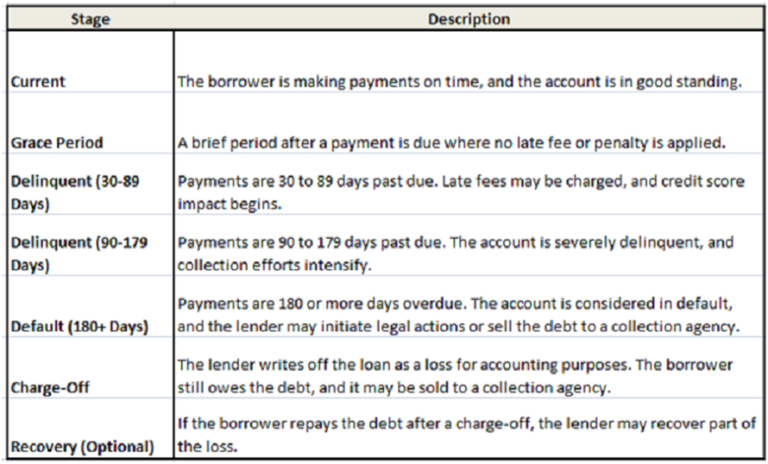

The different stages that loans go through.

Threats:

- The value of mortgaged assets. We have looked at this here, as we believe that the prices of newly built properties will fall. This fully exposes the small banks which have them in their balance at loan value.

- The interest rate rises, the economic slowdown they cause, the first companies to be exposed are the small ones, with less support and political contacts than the big banks.

My former boss would call this combination a ‘nuclear shit swamp’.

Needless to say, he would never buy a company exposed to this ecosystem, even if it was run by Superman.

Setups: Choice of vehicle. From macro and micro to trading.

Weakness:

- Small banks,of course, but with a known central bank reaction function. Basically “one window to save them all’.

- New property prices threaten the whole system. Small banks, big banks, you name it. If assets were to fall below the value of loans granted, there would basically be a massive return of houses to creditors who in some cases securitized the loans and in others did not.

- The debt of small and medium-sized companies first, and the price of their shares last.

The setup derived from this analysis can be found in the next article of the site.

As always and for the 1000th time, these are not trading recommendations. It is our procedure for putting together a technical setup, which we make public for marketing purposes.

See you soon. You can find us at X

We will be in touch.

Martin

Sources:

1.Data sources used

1.Federal Deposit Insurance Corporation (FDIC):Quarterly and annual bank performance reports. Loan portfolio information for banks of different sizes.

- Federal Reserve Economic Data (FRED):

Macroeconomic statistics related to bank lending, including categories such as CRE, C&I, and agricultural lending.

3.Office of the Comptroller of the Currency (OCC):

Supervision and analysis of the performance of national and regional banks.

4.American Bankers Association (ABA):

Reports on banking trends, including the composition of loan portfolios.

5.Federal Financial Institutions Examination Council (FFIEC):

Data on the distribution of loans among small, regional and large banks.