In the weekly report, we outlined that credit risk was starting to emerge, building on top of duration risk that is already clearly priced into the market.

In just four days, rates adjusted sharply and violently. That kind of move naturally forces a valuation reset across assets.

The key question now is not about rates — that adjustment is largely behind us. What we need to determine is whether credit risk is being priced, and more importantly, where it is concentrated.

From there, the framework becomes straightforward:

either we position for a continuation of the duration trade, or we shift decisively into a credit risk trade — depending on what the market is actually pricing.

The causality between Duration and Credit risk

When rates rise — particularly in the case where the main driver is higher inflation expectations — the cost of credit increases.

That alone is enough. When the move is large and fast, it directly pressures business models that rely on financing, increasing the probability of default.

Duration to Credit path

Right now, we are moving through a transition where rate risk is morphing into credit risk. This is not a binary shift. It is a continuous gradient that intensifies as higher financing costs begin to filter into the real economy.

That is the framework, the context we are living in.

Duration trade vs. Credit risk trade.

• QQQ is the purest duration trade. Long-dated cash flows with no direct exposure to credit risk. As rates moved higher, QQQ underwent a valuation reset. However, from a technical standpoint, it has not confirmed a bearish breakdown.

• Financials, on the other hand, are the expression of credit risk. And here, the signal is clear — a technically confirmed bearish breakdown over the same timeframe.

Duration trade vs. Credit risk trade — and their correlation to the 2-year yield

• The rate move over the past four days pushed QQQ’s correlation with the 2-year yield to extreme levels, around -2σ. That is statistically stretched. And yet, QQQ has not confirmed a technical breakdown.

• The same move in rates triggered a clear bearish break in financials. The difference is key: their correlation with the 2-year sits closer to -1σ — roughly half the magnitude seen in tech.

Conclusions

• Financials are less sensitive to rates than tech, yet the drawdown is deeper and technically confirmed.

• That asymmetry matters. It tells us, the market is pricing something beyond duration into financials.

Duration to Credit is a continuous gradient, not a conclusive stage

Validating the shift — and what to watch in HYG

If the risk is transitioning from duration to credit, HYG becomes the confirmation layer. Not the signal — the confirmation.

At this stage, we cannot yet confirm a full transmission into the second phase of Stage 2.

Technically, validation comes with a breakout of the pennant to the upside. The inverse scenario occurs if the breakout is to the downside. Important: the pattern provides a timing window for resolution in either direction — June 2026.

That matters — because it constrains positioning. For now, the trade remains concentrated in XLF. This is not broad credit yet. It is localized stress within financials.

Financials

Within the sector, there are weaker vehicles — such as Wells Fargo (WFC) and Bank of America (BAC) — which, of course, we have already been trading for some time and have published in the service.

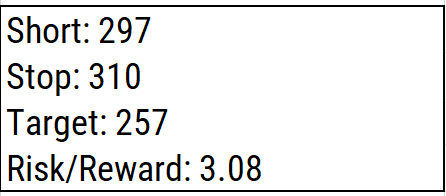

However, this has been the cleanest technical setup we found this week JPMorgan (JPM)

Trade Box

This is the work we do — the framework our subscribers

receive.

If you believe this is an error, please contact the administrator.