A simple week does not define a regime — it operates within it. To properly understand what unfolded over the past one, we cannot lose sight of the monthly environment currently shaping the market.

We are moving through a month where activity reached extreme levels across all asset classes, with the exception of equities.In the past week, activity has started to decelerate — from and still, in high levels.

Capital Flows for the Month: Going Deeper

Capital, of course, flows out of some categories and reallocates into others. Once we segment those categories one level deeper, the flows become crystal clear.

The origin of these flows into the dollar comes primarily from the bond category. The key detail is that this flow did not distinguish between duration or credit quality—it was broad-based for the month.

Capital Flows weekly timeframe

Of course, markets have trends within larger trends. When we look at the last weekly trend in bond credit quality, we come across this.

Activity in high-grade bonds is at absolutely extreme levels—nearly double the activity seen in junk bonds (which also experienced extreme activity). The key difference lies in the fact that flows into quality led to accumulation, which in turn generated positive returns.

This did not happen in junk bonds. They saw very high volume, clearly driven by both inflows and outflows, yet barely managed to generate a positive return for the week. This is a clear message.

Credit quality matters, as the probability of defaults is rising.

SJB: ProShares Short High Yield

Until now, risk was mostly tied to interest rates (duration). Now a new layer of risk is being added to the existing one: default risk.

The path of rates that is currently priced in

The speed of the market shift has led to a situation where, in just two days, expectations moved from a potential rate cut in July 2026 to no cuts until October 2027, even with a slight probability of a rate hike.

Expectations for rate cuts have been pushed back by 15 months, triggering the corresponding repricing in valuations. A strong inflation report and a constrained Fed ultimately tipped the balance.

A 15-month repricing in rates compressed into just a few weeks is not a common occurrence.

Flow Tracking

- Weekly activity across all categories has decelerated relative to the magnitudes observed over the month.

- On a monthly basis, flows showed record activity across all asset classes, with the exception of precious metals.

- All categories posted negative returns over the month, except for USD cash and crude oil.

- These two assets acted as a vacuum for equity capital flows.

- On the monthly timeframe — the one that defines the regime — the shift into cash did not differentiate by bond type. High grade, high yield and all segments of the curve experienced equally strong outflows.

- In the past week, activity in bonds by credit type remains elevated, but the directionality has shifted toward higher-quality credit.

- This is the most important signal: risk perception has transcended duration and is now aggressively pricing credit failure. This is the new regime.

Capital flows and the real economy

In just a few days, the narrative shifted from a tug of war between a slowing economy with controlled inflation — and the real prospect of near-term rate cuts — to an economy facing strong inflation, now coupled with declining disposable income as a direct consequence of rising oil prices which in turn increases the probability of defaults.

Naturally, this has a direct impact on valuations across the board — particularly on assets with the highest sensitivity to interest rates and poor credit quality.

Capital Flows and the cascade effect

As highlighted in previous reports, there were two sectors particularly exposed that had already begun adjusting ahead of this shift for several internal reasons.

Financials

Construction

The difference now, is that the macro chain reaction is starting to propagate across the rest of the sectors.

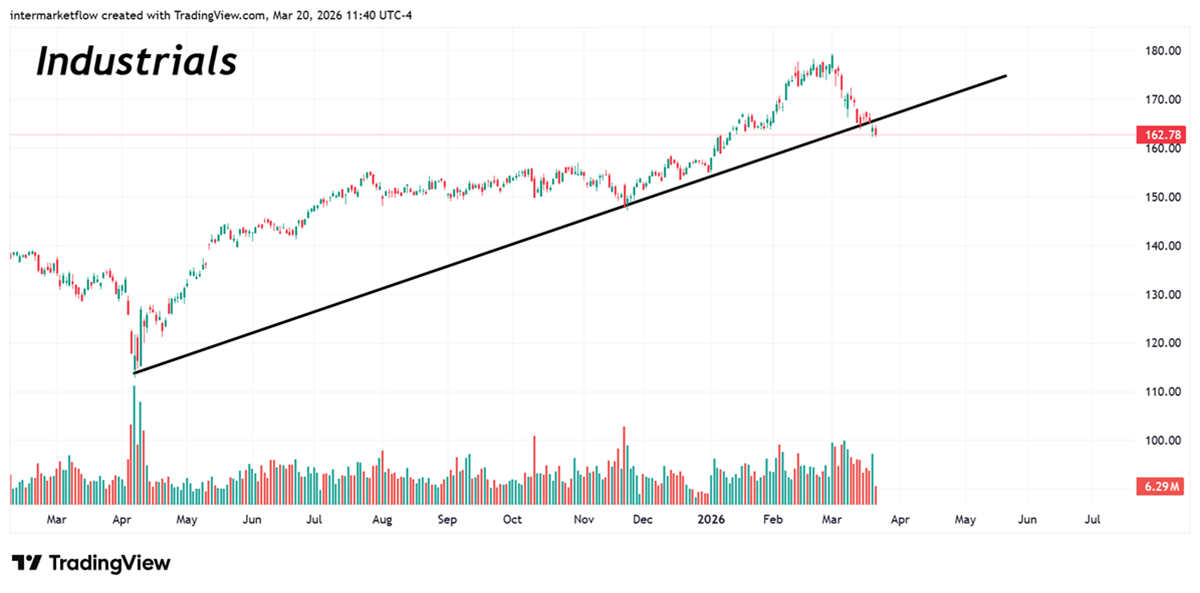

Following construction — as expected — materials

Capital flows and the new Regime

It is a unidirectional and extreme volatile environment — an exceptionally dangerous one. A shift in the news flow, a sharp drop in oil, or simply a better-than-expected CPI can trigger violent fluctuations but not a trend change direction.

Those fluctuations are the opportunities. The damage to the real economy runs deeper than a single CPI print or a pullback in oil.

Conclusions

- Short beta in the opportunity zone! High volume breaks like this need a short squeeze before they continue.

- Short Low Quality across the board. Bonds, Equities and Emerging Currencies.

- We do not front-run the dollar reversal. While we wait for that structural pivot, our focus remains exclusively on tactical short execution.

Invalidation zone #1

Trade in opportunity land. Don´t chase the price.

Invalidation zone #2

This is where we close the framework. In the Mid-Week report, subscribers will receive the specific vehicles and our tactical setups to trade this environment.

If you believe this is an error, please contact the administrator.