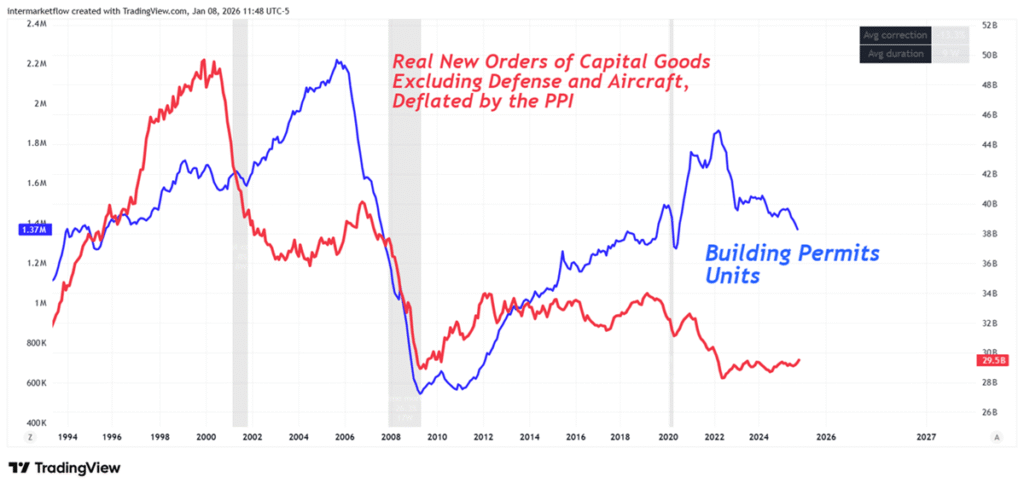

#89 New Orders: Nominal Strength, Real Weakness

New orders can be misleading. We analyze the nominal trap through building permits and intermarket, intramarket and speculative capital flows.

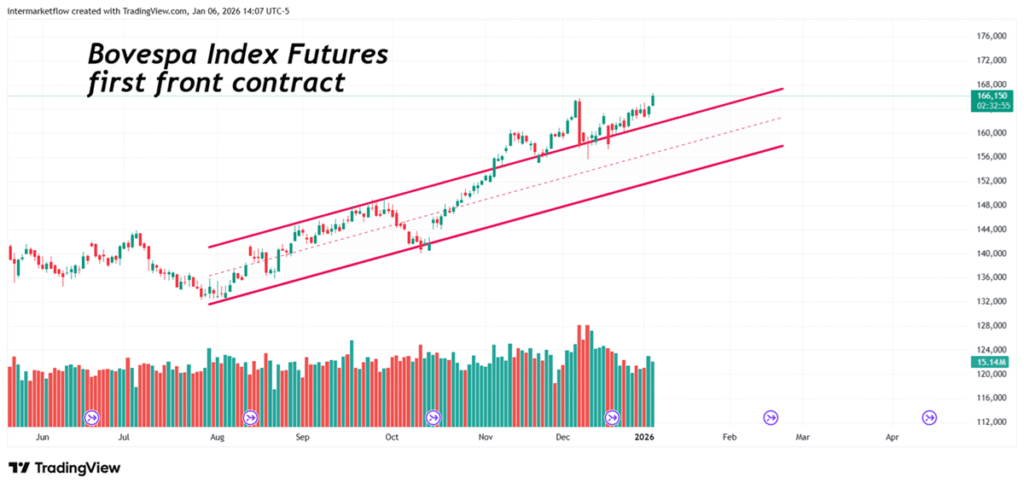

#88 Trading Emerging Markets: Brazil

An intermarket analysis of Brazil and emerging markets, exploring yield curves, FX risk, carry dynamics, commodities flows, and their role as long-term portfolio diversifiers in a shifting global macro environment.

#87 Intermarket Flows and Early-Year Market Signals

Intermarket Flows: We analyze capital outflow and inflow hubs, seek risk-efficient operating environments, and examine currencies and commodity-intensive economies.

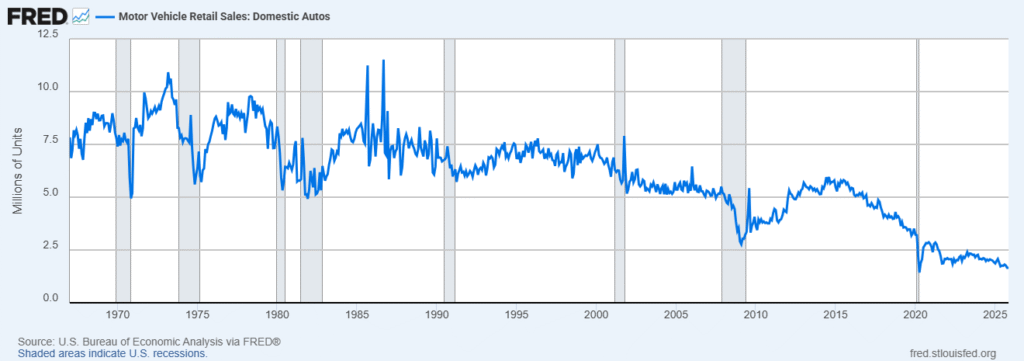

#86 Macroeconomics, rates and the Automotive Sector

We analyze the evolution of auto credit and vehicle sales, and how short-term interest rates directly impact demand. We place today’s sales levels in historical context and examine five vehicles within the auto retail sector.

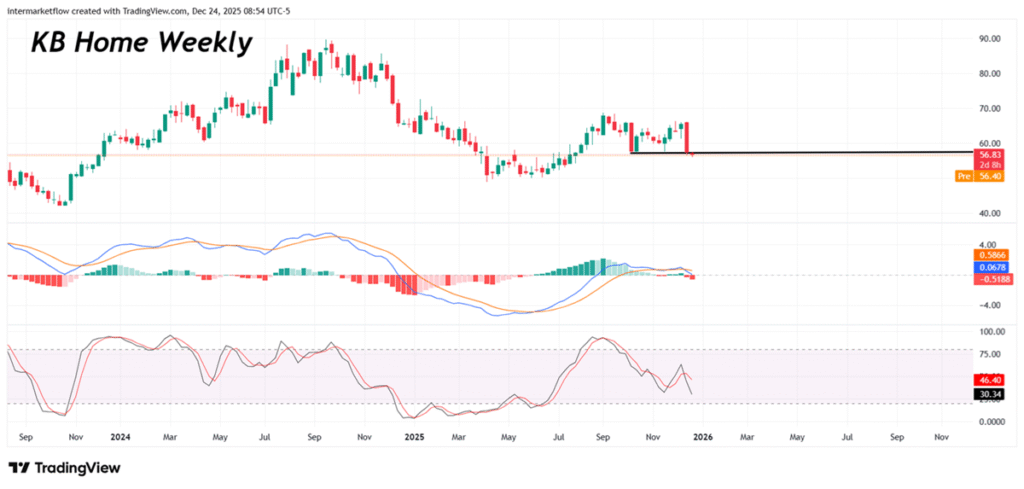

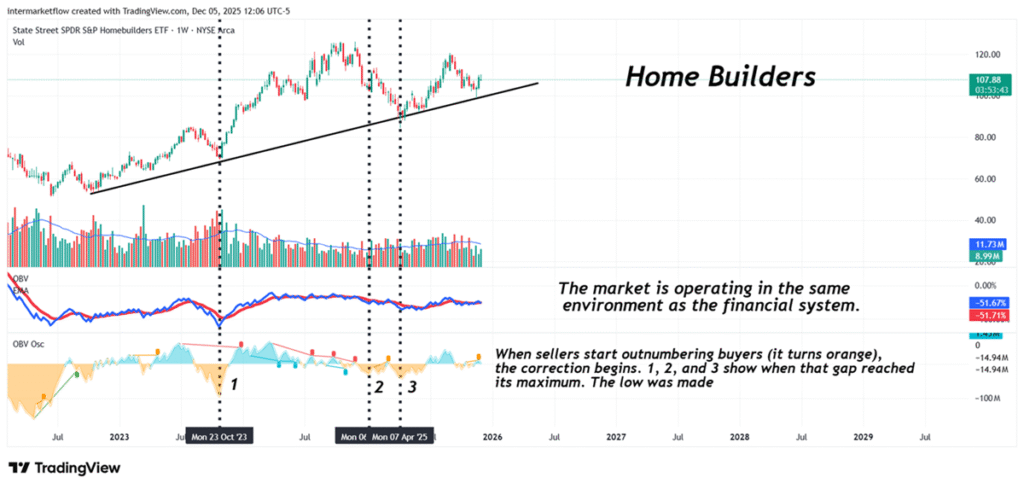

#85 The Real Economy: Winners, Losers, and Injured Players

The real economy and the context we are trading today.The VIX: a historical perspective on current levels, with a specific comparison to the Dot-com and GFC recessions.The real economy and divergent reactions within the financial and homebuilding sectors.

Intermarket flows: the same winners remain in control.Intra-market analysis: segmentation to see what headline data hides.The health of the AI trade.

Sector-by-sector relative performance versus the S&P 500.

Relative strength within the homebuilding sector, identifying specific vehicles.

Home Depot and KB Home: wounded prey on the open plain.

#84 The discretionary delusion and the market’s stance. Three vehicles to track.

We break down retail sales and why Consumer Discretionary is completely detached from reality. We picked three vehicles to go deeper, while tracking how risk-takers positioned themselves this week.

#83 Unemployment, Macro Cycles and Sectors

A historical perspective on unemployment—its levels and the current trend relative to past cycles. Its connection to sectors, and how sector leadership evolves as the cycle matures. We then zoom in on two sectors in search of vehicles to trade.

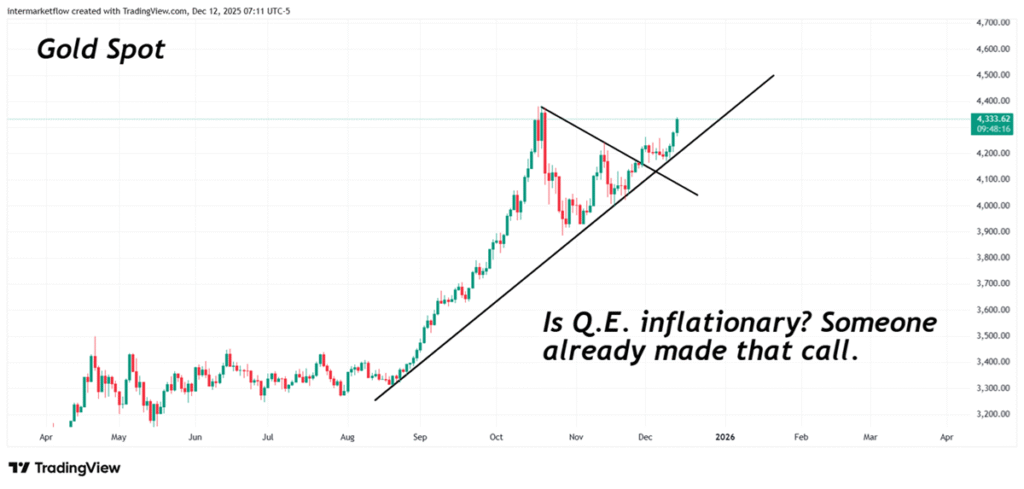

#82 QE and inflation. A popular debate with no real substance

QE and inflation is one of the most popular debates in macro—and one of the most misunderstood. In plain language, QE is the Fed buying bonds and paying with bank reserves: they hit “enter” and reserves show up on a bank’s account at the Fed. The real question isn’t whether that money “exists.” It’s what the second-round effects are—especially when QE ends up supporting the Treasury market that finances the fiscal deficit.

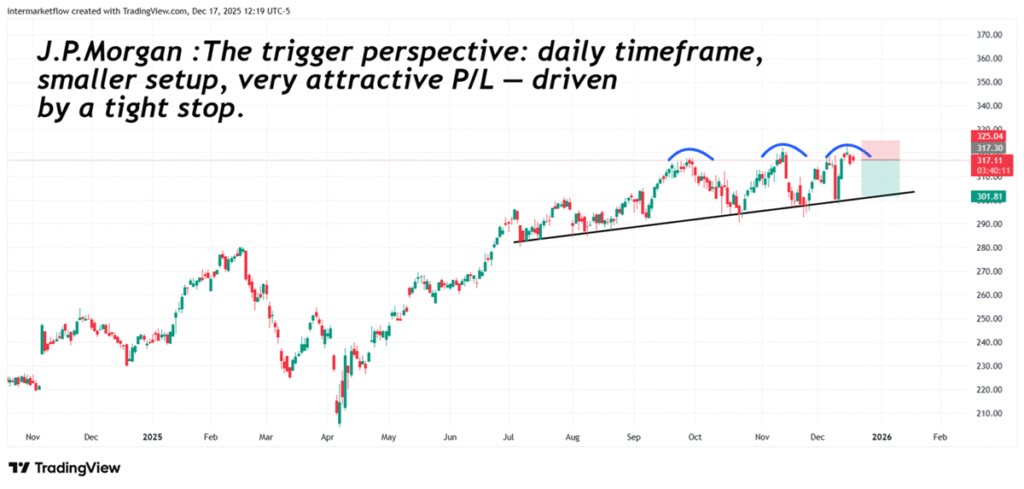

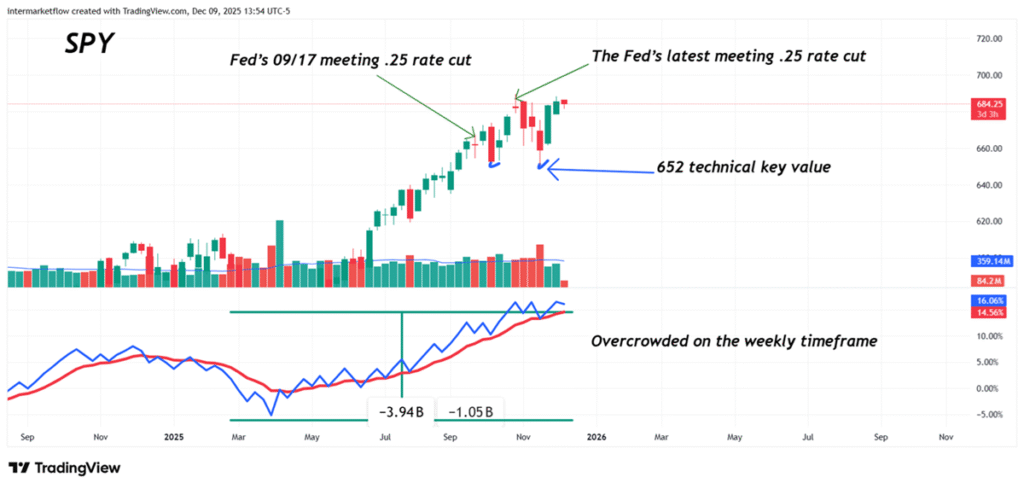

#81 Feed meeting: On your marks, get set… go

The Fed meeting is acting as the catalyst. Here, I read the messages the S&P 500 is sending across different timeframes. Too clear not to hear.

#80 End of QT ≠ QE.

We analyze the end of QT and the rate cut scheduled for next December 10. Which mechanisms must reactivate for it to transmit into the real economy, and the scenarios ahead. Why we believe we could see a “buy the rumor, sell the news” into Wednesday, and the three stages of a correction scenario.