Another week has passed, and the market keeps sending a clear message, which is basically, that it has nothing clear.

Intermarket: The Big Four

A fragmented signal

- U.S. equities and bonds did not show a major regime change this week relative to the monthly situation.

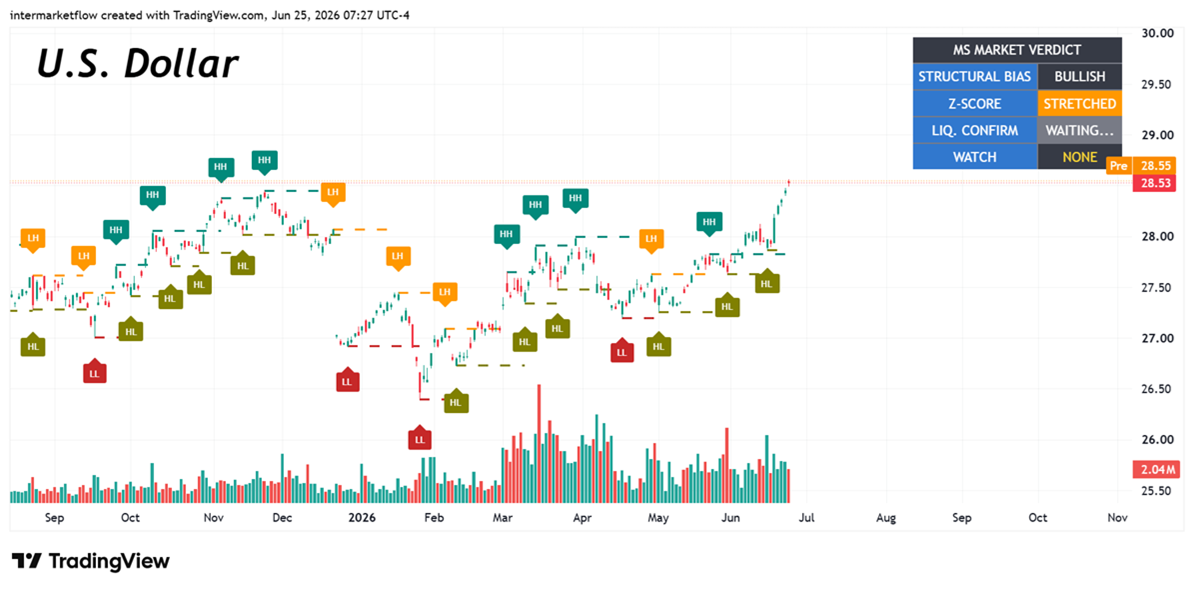

- The U.S. dollar continues to be the only one moving in spite of weak participation.

- Gold shows the sharpest reversal from the prior monthly condition, aggressive distribution flows finally slowed down from the stampeded out we saw last couple of weeks.

Overall, capital is not rotating into a clean risk-on or risk-off regime. The market remains in transition, with weak participation and no dominant flow confirmation. U.S. Dollar was main destination for weekly flows.

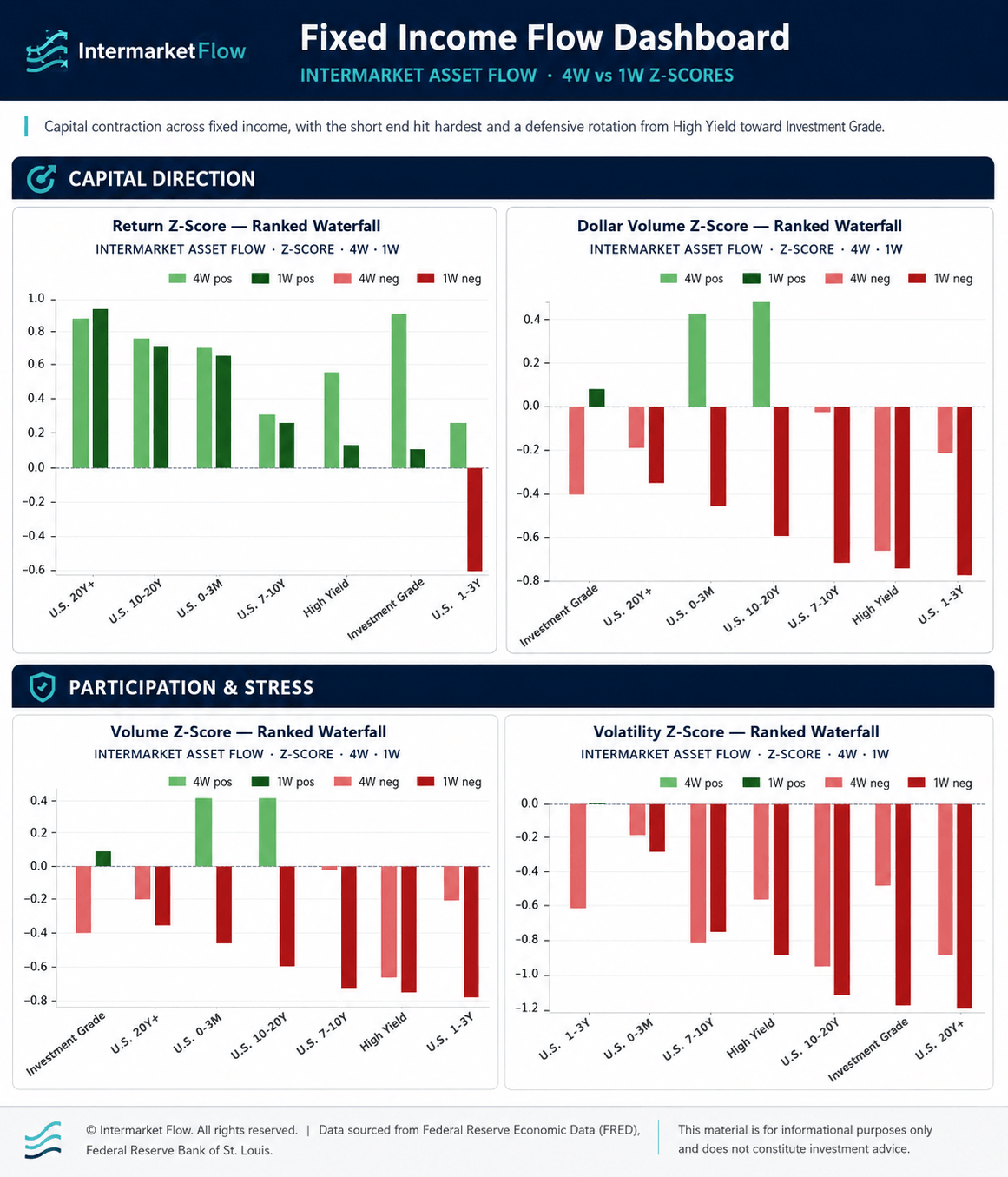

Fixed income shows capital contraction

Volume and Dollar Value weakened broadly, while volatility also compressed. Even in this context, we can still extract valuable information.

- The key signal came from the front end of the curve. U.S. 1–3Y was the weakest segment, combining negative weekly returns, falling volume and weaker Dollar Value.

- The short end did not behave as a safe parking area. Instead, it became the part of the curve where uncertainty was expressed most clearly.

- Long duration held up better in price terms, but the move lacked flow confirmation. U.S. 10–20Y and 20Y+ still posted positive returns, but participation faded, which makes the price strength less convincing.

- Credit quality also separated sharply. Investment Grade was the only segment with higher weekly volume, while High Yield saw a deeper volume decline. That points to a defensive rotation inside credit rather than a broad accumulation of fixed income risk.

Key points

- Capital contracted across fixed income, but the pressure was not uniform. The weakest point was the short end of the curve.

- Credit flows rotated defensively away from High Yield and toward Investment Grade.

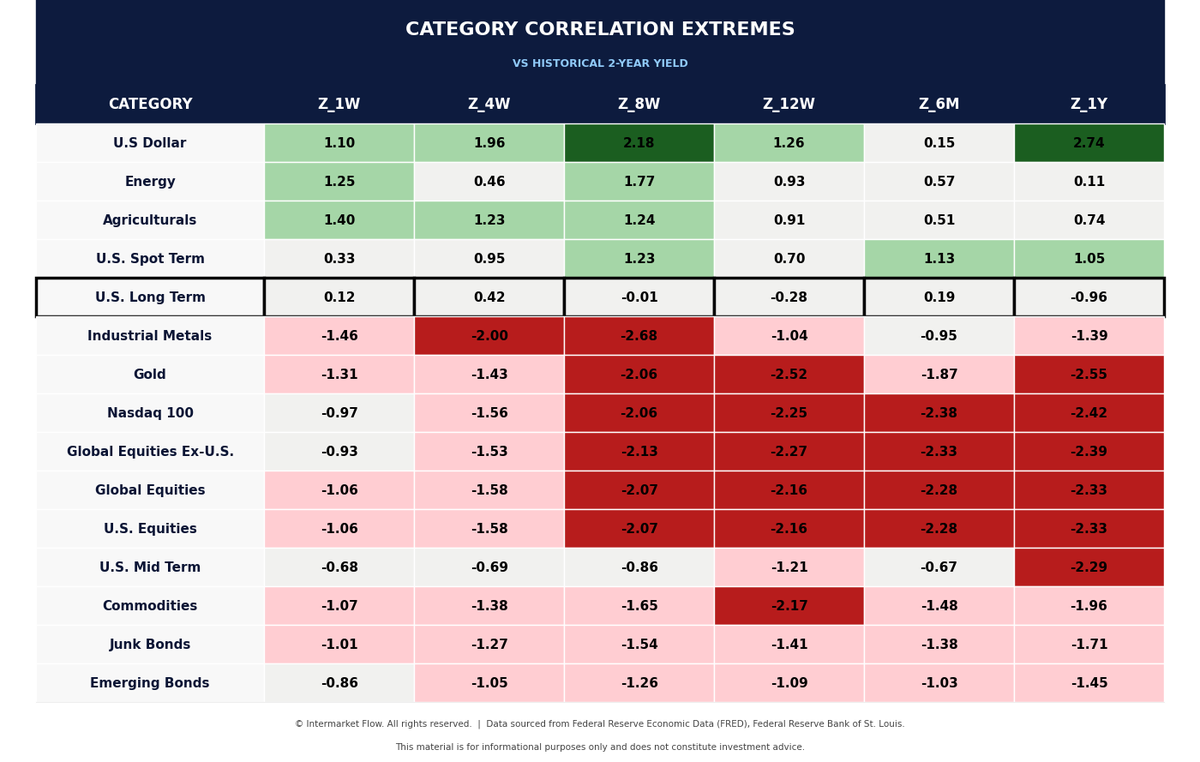

2-Year Yield — Monetary Pressure

- The 2Y is a monetary tightening signal, not a growth signal.

- Positive correlations are concentrated in U.S. Dollar, cash-like assets, Energy and Agriculturals.

- Negative correlations are concentrated in Gold, equities, credit and emerging bonds.

- The message is clear: higher front-end rates support dollar/liquidity, while pressuring risk assets.

- The 2Y is a monetary tightening signal, not a growth signal.

- Positive correlations are concentrated in U.S. Dollar, cash-like assets, Energy and Agriculturals.

- Negative correlations are concentrated in Gold, equities, credit and emerging bonds.

Key point

- When the 2Y rises, the market is not buying growth. It is buying liquidity, dollar strength and protection against monetary pressure.

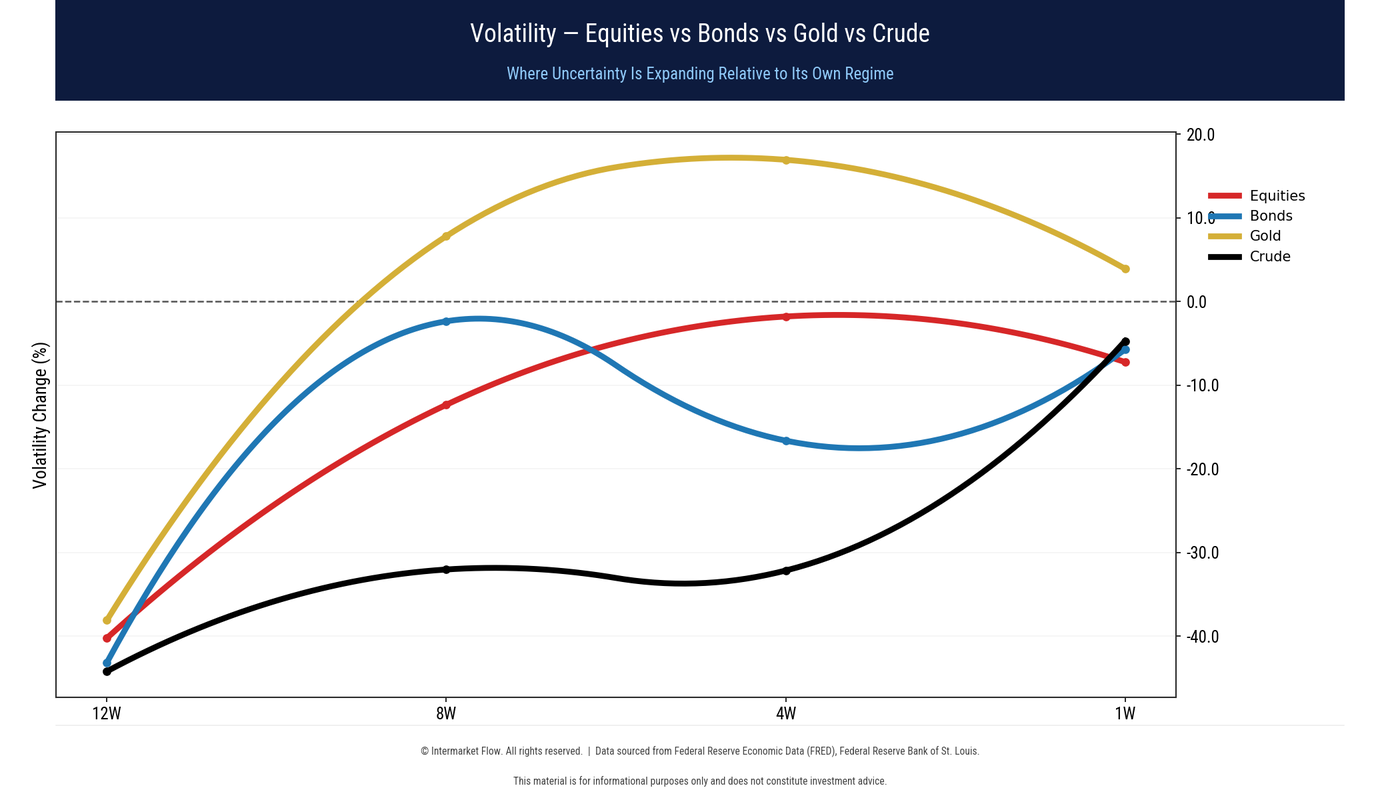

Cross-Asset Volatility

- Volatility is no longer uniformly compressed.

- Equities remain contained.

- Bonds are normalizing after leading the previous stress phase.

- Gold is easing from its volatility peak.

- Crude is the only asset showing a sharp late rebound in uncertainty.

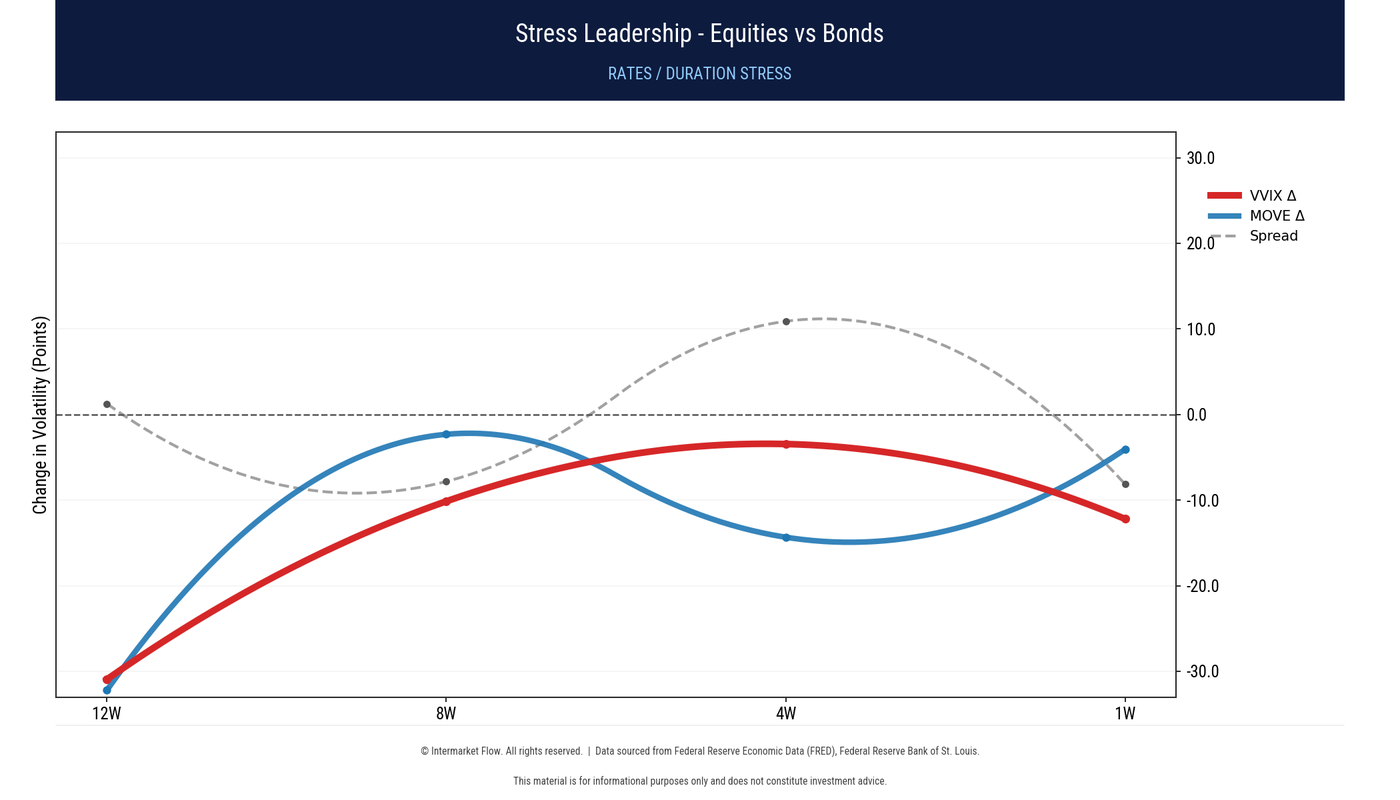

Stress Leadership

Rates led the stress, not equities. The MOVE/VIX spread widened during last week , but equity volatility has still not priced this.

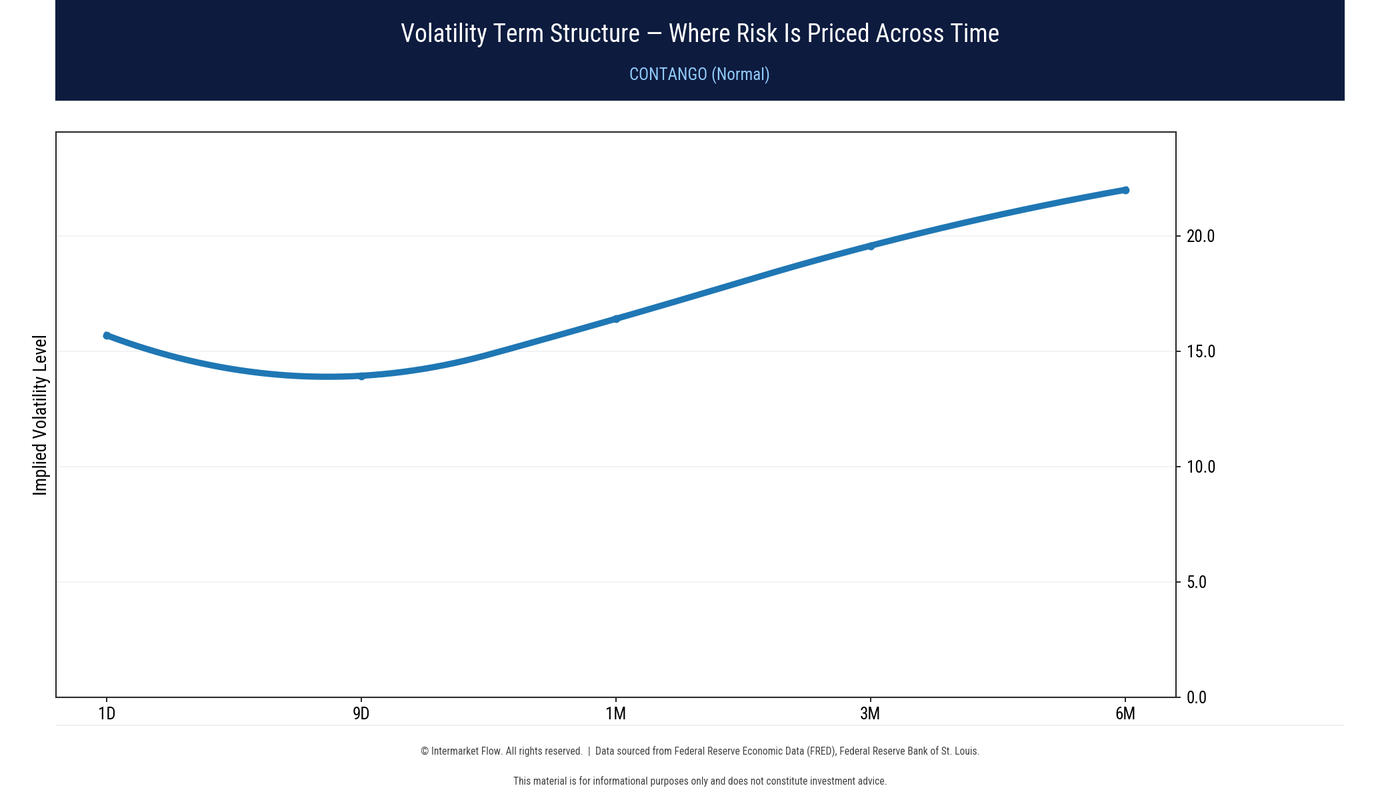

VIX Term Structure

The VIX curve remains in contango. That means the market is not pricing immediate equity panic, but it is still assigning more risk to future windows than to spot volatility.

Volatility

Volatility is not confirming a panic event, but the compression phase is no longer clean.

The first signs of stress appeared in rates, while equity volatility remains subdued. Crude is starting to show late-cycle uncertainty, and the VIX curve remains in contango. That means the market is not yet pricing a full shock, but the internal message is clearly more fragile.

The broader structure confirms that reading. Monetary pressure remains high, fixed-income flows are contracting, equities are weak without volume support, and rates are behaving more like a tightening shock than a growth signal.

Bottom line: there is no capitulation yet, but internal deterioration is clear. The market is fragile, defensive, and exposed to repricing if volatility stops staying contained.

Trading

- Stay defensive. This is not a confirmed panic regime, but it is also not a healthy risk-on setup. Keep gross exposure controlled and avoid adding broad beta until volume and Dollar Value confirm.

- Do not chase equity rebounds. U.S. equities remain weak, with low volume and no material improvement in flow structure. Any bounce without participation should be treated as an opportunity to reduce exposure, not as confirmation of a new leg higher.

- Prefer liquidity over risk. Cash, T-Bills and short defensive liquidity still matter, but the short end is showing stress and capital contraction. Use liquidity as protection and optionality, not as a signal that the market is safe.

- Be selective inside fixed income. Long duration has held prices better, but without strong flow confirmation. Investment Grade is preferable to High Yield. Avoid increasing High Yield exposure until volume, Dollar Value and price action confirm renewed credit appetite.Do not short volatility aggressively. The VIX curve remains in contango, but cross-asset volatility is no longer uniformly compressed.

- Stress already appeared in rates and is rotating across assets. Short-vol trades have poor asymmetry here.Use hedges while volatility is still contained.

- Equity volatility has not fully priced the internal deterioration. Put spreads or downside hedges on equity beta remain attractive while spot vol is still contained and before a broader repricing.

- Watch the key triggers. A break in High Yield, renewed MOVE expansion, rising VIX front-end, or a volume-backed equity selloff would shift the setup from fragile correction to active risk-off.

Bottom line: keep risk light, fade low-volume equity strength, prefer liquidity and quality credit over High Yield, avoid short-vol exposure, and use contained volatility to maintain downside protection.

Risk Takers

In a market where rates are driving the cycle, the right vehicles are the ones with the highest sensitivity to rates. That means long-duration equities, high-multiple growth, small caps, long-duration bonds, and rate-sensitive credit.

The setup is not to chase weakness blindly. The opportunity is to identify assets that are still holding up on poor participation, because those are the areas most exposed if rates keep tightening or volatility reprices.

Intermarket Flow

If you believe this is an error, please contact the administrator.