A Technical Correction With a Liquidity Warning

We delayed the release of the Mid-Week Report to give prices enough time to digest yesterday’s CPI data.

Brief check to determine whether the conclusions we reached on Sunday still hold.

Market Regime: Changes Since Sunday and Confirmation of the Monthly Time Frame

- Not only did the structure not change — including yesterday’s data, it actually strengthened.

- Market regimes have moved into the Distribution quadrant across both Dollar Value and Return.

- Looking at volatility and volume, the exit from risk assets came with significant participation, which reinforces the core hypothesis: the volatility compression phase is over, exactly as we have been expecting for roughly the past two weeks.

- There is liquidation. Risk On is being invalidated. Risk Off is not being validated. And the market is still not pricing credit risk.

Same situation as Sunday — only more pronounced.

The Week in Detail: Return, Volume, and Volatility

- We are in a correction with participation, but without destination.

- The focus is the closing of risk positions, especially High Beta exposure.

- The two previous stress events we saw in the bond category have now migrated into equities.

- Gold’s behavior — declining while volume and volatility expand sharply — does not support the idea of a clean Risk-Off rotation. It suggests that Gold is being used more as a source of liquidity than as a safe-haven destination, likely to reduce or cover leveraged exposure elsewhere.

Volatilidad describing clearly markets opinions

Interpreting a Technical Correction

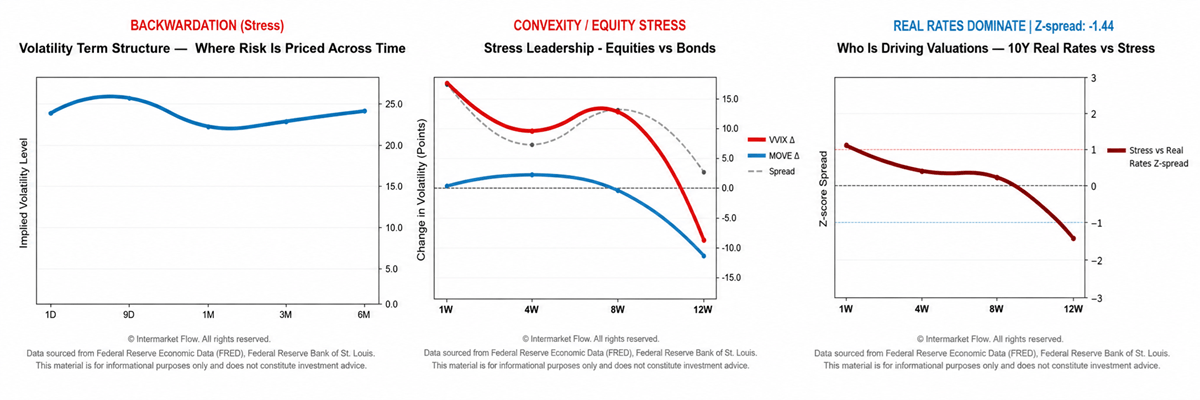

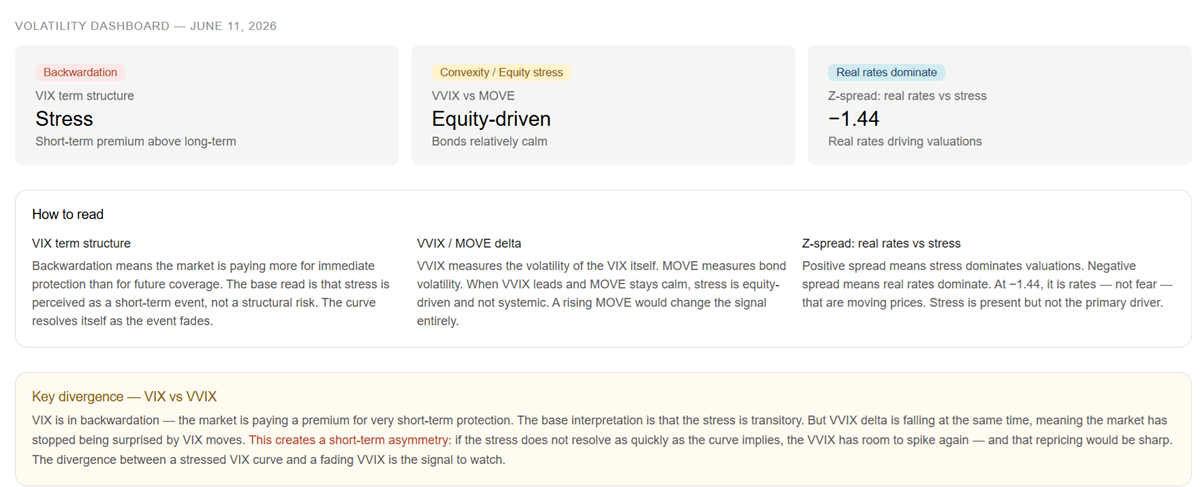

- The asymmetry between expected volatility and the short-term cost of protection reflects how the market is currently framing the event.

- For now, this is being treated as a corrective move without clear follow-through. Valuation pressure is being driven mainly by rates, not by a broad repricing of corporate fundamentals or a full shift into risk aversion.

- The source of uncertainty remains inflation, not the operating performance of companies. That distinction is critical because, with inflation data still uncomfortable and labor data showing resilience, the probability of a near-term Fed pivot is not part of the current base case.

As long as the market treats rates as an operational inconvenience, the correction can remain technical. But if the focus moves from inflation uncertainty to policy constraint, the repricing can become more unstable: the Fed has less room to cushion the downside precisely when risk assets may need it most.

Operational Recommendations,Risk Management

- Fade High Beta rebounds.

- Treat bounces as exit opportunities, not accumulation.

- Tighten dynamic stops across unhedged long risk exposure.

Asymmetric Protection

- Near-term hedging remains relatively cheap versus the cross-asset stress signal.

- Use 30–45 day put structures for portfolios that still need risk exposure.

- Protection should be added before MOVE, VVIX, or credit spreads reprice higher.

Liquidity

- Raise cash / T-Bill exposure. Liquidity is both protection and optionality.It hedges a shift from technical repricing into structural stress.It also preserves dry powder for opportunities created by capitulation.

Watch MOVE and High Yield spreads

A disorderly jump here would confirm a shift from technical repricing into operational / credit stress.Until then, the market is still treating the event as a rate adjustment.

Core Message

- Risk On is invalidated in the short-term structure.

- Risk Off is not validated.

- Gold is being used as a source of liquidity.

- The priority is protection, liquidity, and disciplined exit management.

Intermarket Flow

If you believe this is an error, please contact the administrator.

P.S.

For those whose free trial ends today, this is your final report.

Over the past days, you have seen the full IntermarketFlow framework in action: capital flows, regime signals, volatility, credit, risk appetite, and the structural divergences developing beneath the surface.

If this helped you understand the market beyond price action, you can keep full access to the framework here.