Intermarket: Inside an Expected Correction

This was not a classic rotation into safe-haven assets.It was not an equity selloff being recycled into bonds, and it was not capital hiding in gold.

What we saw was a broad position unwind: forced profit-taking driven by a correction in rate expectations and by the impact that higher rates can have on future economic growth.

That distinction defines the trade.

- This is not a credit crisis. Not yet. There was no clean discrimination by credit quality, duration, or defensive profile.

- Bonds failed to provide clean protection across the curve.

- Gold failed to absorb the flow.

- Equities, especially Growth and high-beta exposure, took the main hit.

The message is simple: the market is recalculating the cost of capital, reducing exposure, and taking down risk across the board.

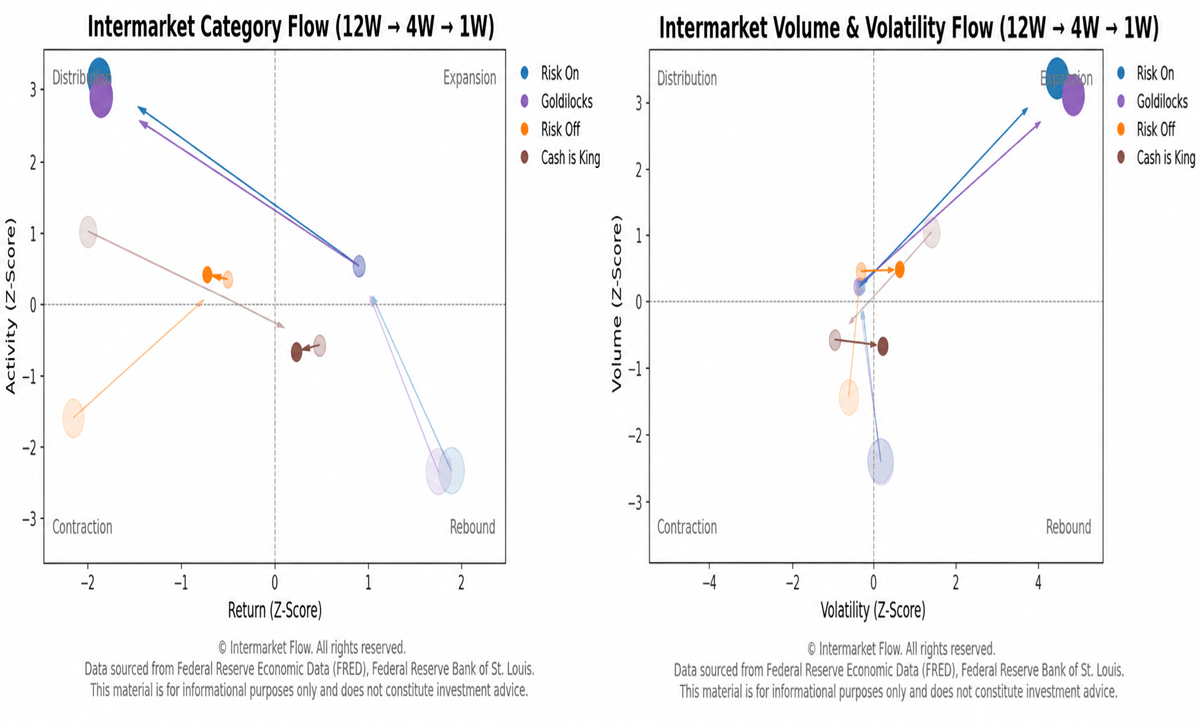

From Risk-On to Risk-Off?

The cleanest way to summarize what happened — especially on Friday — is through the regime structure.

- The correction was concentrated in the Risk-On regime. Everything tied to risk, beta, growth, and multiple expansion was sold aggressively. This was not a mild rotation. It was a sharp unwind of the market’s most pro-cyclical and duration-sensitive exposures.

- But Risk-On did not rotate into a clean Risk-Off regime.

That is the key point.

Inside the Equity Correction

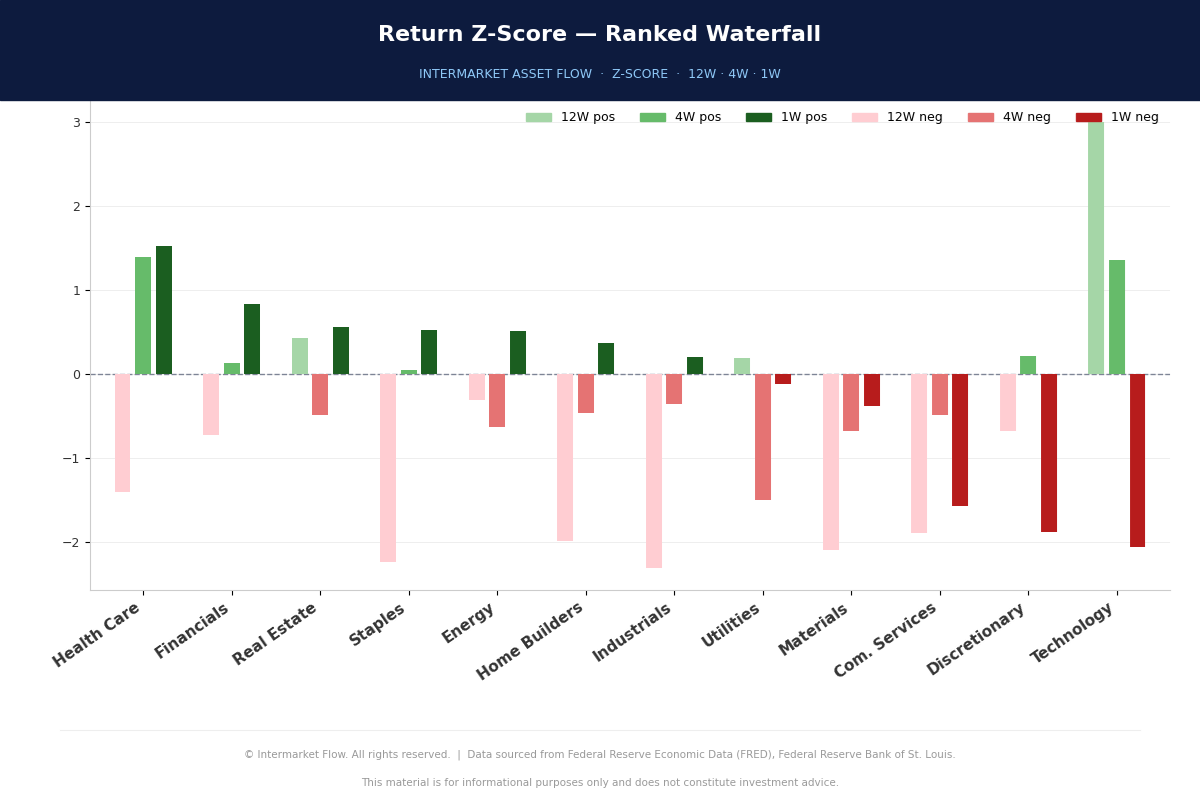

The equity correction was not uniform. It was a clear internal rotation away from duration-sensitive growth and into defensive, lower-beta sectors.

- Technology had been one of the strongest relative leaders over the 12W and 4W windows, but in 1W it became one of the weakest sectors versus the S&P 500. That is not a pause. It is a sharp loss of relative momentum in the market’s main leadership engine.

- On the other side, Health Care, Financials, Real Estate, Staples, and Home Builders showed better relative performance. The market rewarded defensive exposure, value, and sectors that can benefit from rate stabilization, while punishing expensive, high-multiple assets.

- Discretionary, Communication Services, Materials, and Technology remained on the weak side. That confirms the correction was concentrated in growth, multiples, and beta — not across equities equally.

The central message is simple: the S&P 500 is correcting, but beneath the surface the market is rotating internally. It is not abandoning equities uniformly. It is dismantling Growth leadership and looking for relative shelter inside the equity market.

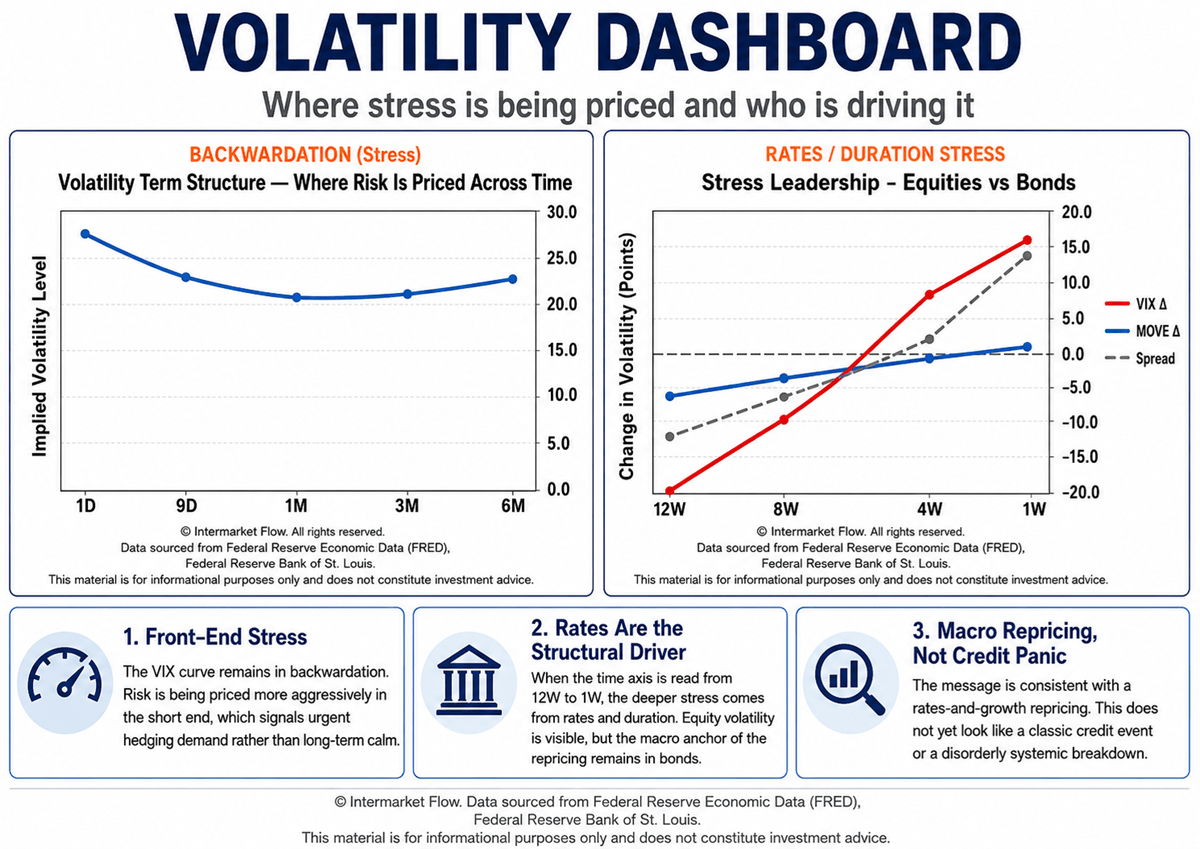

Volatility Confirms the Shift

- The market is pricing volatility today, not a sustained shock across the entire curve.

- The short end is stressed, but the structure does not yet suggest a continuous volatility regime.

- The key change is that equities finally came out of complacency.

- Equities had absorbed two previous volatility shocks from the bond market without a full adjustment. That changed this week.

- The correction is now being led by equities. Bonds triggered the first warnings, but equity risk is now doing the repricing.

- This matters because the market is no longer ignoring the pressure from rates. Growth, beta, and high-multiple assets are now adjusting to the same macro shock that bonds had already been pricing.

Course of Action

1. Do not buy the dip in Tech/Growth yet.

The current regime is deleveraging, not rotation. Growth, Nasdaq, U.S. equities, and global equities are absorbing the bulk of the liquidation, with volume at climax levels. As long as Z_VOL remains above 2.8 and volatility remains elevated, there is no evidence of a durable floor. Buying before the VIX curve normalizes and VVIX stops leading stress is catching the knife.

2. Cash and USD are active positions, not inaction.

This is not a classic “sell equities, buy bonds” regime. Gold and bonds failed as clean safe havens, while the VIX curve remains in backwardation, meaning the market is overpaying for immediate protection. Until the curve returns to contango and short-end volatility pressure fades, liquidity is the trade. USD remains the only relatively clean defensive asset with positive return behavior across short and longer windows.

3. Avoid long duration; bonds are not confirming protection.

There is no flight-to-quality in bonds. Selling pressure is broad across duration and credit quality, which points to rates and growth expectations repricing, not credit panic. Long-duration exposure remains vulnerable. If already positioned in long bonds, this structure argues for reducing exposure or staying tactical rather than treating bonds as automatic protection.

4. Monitor capitulation risk through volatility spreads and cyclicals.

The key signal is whether VVIX stops leading MOVE and the equity-volatility shock begins to converge. At the same time, watch Industrials and Materials. If those second-line sectors start showing liquidation volume similar to Technology, the correction shifts from a Growth-led unwind into broader systemic capitulation. Until that happens, this remains a macro repricing event — not a credit crisis.

Final Message

The market is not moving through a normal correction.

Bonds did not protect. Gold did not absorb the flow. Growth and high-beta equities took the main hit. This was not a clean risk-off rotation — it was a repricing of rates, growth expectations, and the cost of capital.

Inside the full report, we break down what changed, where the damage is concentrated, and why this correction matters for the next tactical decisions.

If you want to understand what the market is really pricing before the narrative catches up, this is the type of framework we publish at Intermarket Flow.